BUILDING LANDMARKS, CHARTING GROWTH

157

Annual Report 2015

Relevant Guideline or Principle

(as per Code of Governance 2012)

Page

Reference

in this

report

Our compliance

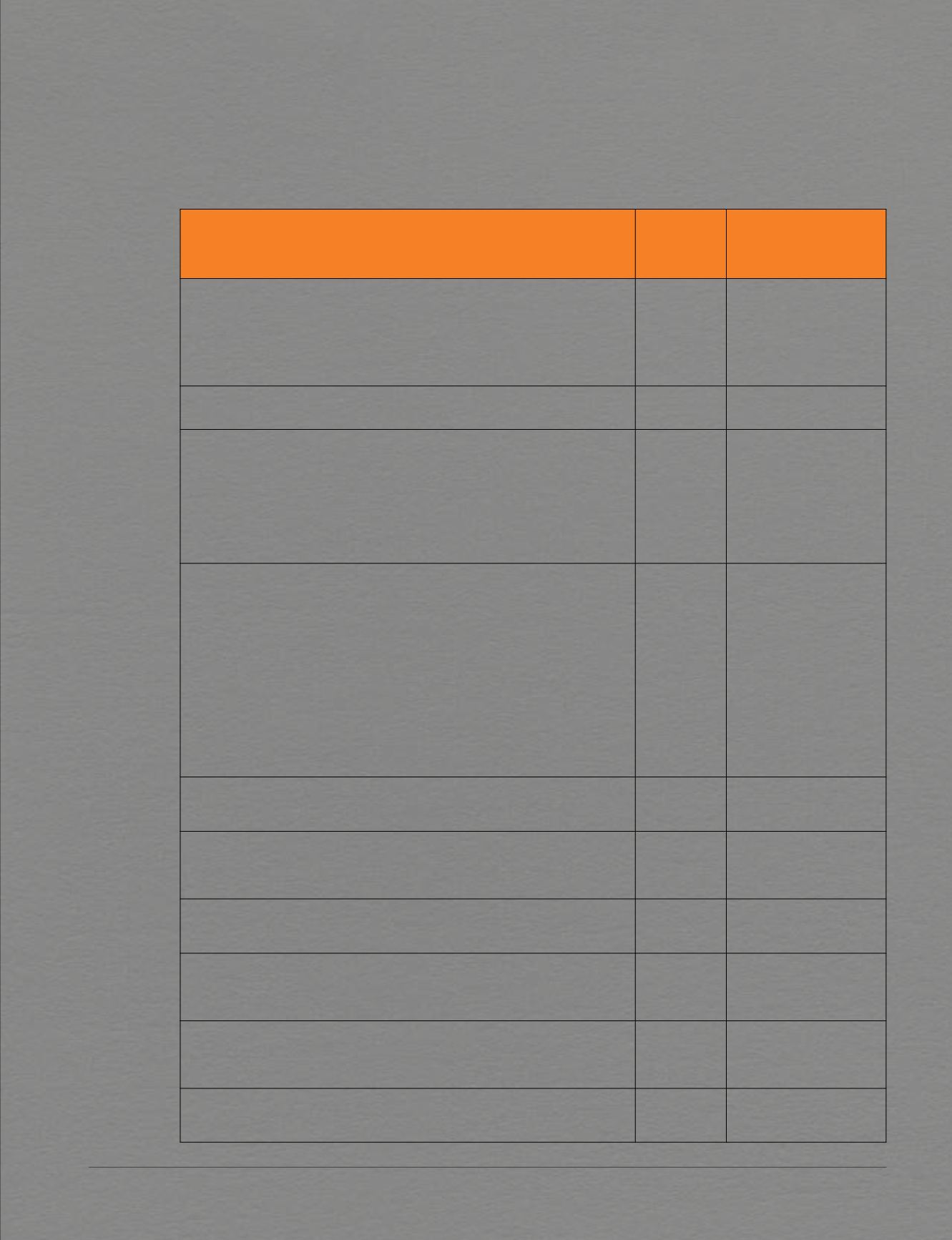

Guideline 9.4

Details of the remuneration of employees who are immediate family

members of a director or the CEO, and whose remuneration exceeds

S$50,000 during the year. This will be done on a named basis with

clear indication of the employee's relationship with the relevant

director or the CEO. Disclosure of remuneration should be in

incremental bands of S$50,000

135

Not Applicable

Guideline 9.5

Details and important terms of employee share schemes

180 to 182,

228 to 230

√

Guideline 9.6

For greater transparency, companies should disclose more

information on the link between remuneration paid to the executive

directors and key management personnel, and performance.

The annual remuneration report should set out a description of

performance conditions to which entitlement to short-term and long-

term incentive schemes are subject, an explanation on why such

performance conditions were chosen, and a statement of whether

such performance conditions are met

135

√

Guideline 11.3

The Board should comment on the adequacy and effectiveness of the

internal controls, including financial, operational, compliance and

information technology controls, and risk management systems

The commentary should include information needed by stakeholders

to make an informed assessment of the company's internal control

and risk management systems

The Board should also comment on whether it has received

assurance from the CEO and the CFO: (a) that the financial records

have been properly maintained and the financial statements give true

and fair view of the company's operations and finances; and (b)

regarding the effectiveness of the company's risk management and

internal control systems

139

√

Guideline 12.1

Names of the members of the AC and the key terms of reference of the

AC, explaining its role and the authority delegated to it by the Board

139,

158 to 159

√

Guideline 12.6

Aggregate amount of fees paid to the external auditors for that

financial year, and breakdown of fees paid in total for audit and non-

audit services respectively, or an appropriate negative statement

140

√

Guideline 12.7

The existence of a whistle-blowing policy should be disclosed in the

company's Annual Report

140 to 141

√

Guideline 12.8

Summary of the AC's activities and measures taken to keep abreast

of changes to accounting standards and issues which have a direct

impact on financial statements

141

√

Guideline 15.4

The steps the Board has taken to solicit and understand the views of

the shareholders e.g. through analyst briefings, investor roadshows or

Investors' Day briefings

143

√

Guideline 15.5

Where dividends are not paid, companies should disclose their reasons

143

A dividend has been

declared for the financial

period under review.